Micro, meso, macroeconomics and wealth distribution

andrea.parisi | Published: 8 Mar 2024, 9:38 a.m.

Economics is traditionally subdivided into micro and macroeconomics. The two subdomains cover two different levels of applications of economic theory. The International Monetary Fund website introduces the difference between microeconomics and macroeconomics by comparing it with physics. Physicists study nature at large scale (for instance planets, stars and galaxies) and at small scale (molecules, atoms, and their constituents: proton, neutrons, quarks, electrons, etc). Similarly (according to the International Monetary Fund), economists study the large picture of macroeconomics, which looks at the overall economy at the level of nations (therefore looking at GDP, inflation etc), whereas microeconomics looks at the level of individual markets. The comparison with physics in this context is quite ubiquitous, and if you are a physicist as I am, you are likely to be left confused by this equivalence, because it is not truly appropriate.

The two subdomain of economics would have been better named macroeconomics and meso-economics. In physics we have roughly three level of description: a macroscopic level (for instance if we look at a surface of a table it looks smooth), a mesoscopic level (if we look at the same surface with a microscope we will find irregularities and a rough surface), and a microscopic level (if we look at the same surface with an atomic force microscope, we can resolve single atoms). The microscopic level resolves at the level of the constituents of the object of interest. The equivalent level of the latter in economic theory would be the study of economics at the level of single individuals. The mesoscopic level would average out differences between single individuals, and look at the level of communities. Market level is a mesoscopic description rather than a microscopic description. This is quite evident as the single individual in microeconomic theory is not characterized by its specific curves (its own demand and supply curve for instance), but by generic average-like curves (the demand and supply curves for the market).

Of course, we are dealing with just names: once the meaning of each term is made clear, there is no reason of confusion. However, this subdivision of economic theory into these two subdomains reveals an underlying issue. To avoid confusion and clarify where the issue is, I will introduce an alternative naming for the three different levels I am referring to: high-level economics, market-level economics and individual-level economics. The use of these alternative names will clarify when I am referring to "micro" in the neoclassic sense (thus, market-level economics) on in my own understanding (individual-level economics). Macroeconomics would correspond to high-level economics, while microeconomics would correspond to market-level economics. Individual-level economics is not handled by modern or neoclassic economic theory.

Let me explain the reason behind all this. The naming-convention used in economics (thus macro- and micro- economics) confused me when I first encountered it, because I could not find any connection between the behaviour of the microscopic world (the atoms, thus individual economic actors) and the macroscopic world (the large scale view, the macroeconomic theory). In microeconomics, individuals and individual heterogeneities are completely ignored. Instead, economic theory introduces market averages, thus treating individuals not as individuals, but collectively at market level. As explained above, this is a "mesoscopic" description, so a description belonging to what I call market-level economics. When discussing demand and supply, economic theory produces curves that represent averages over a population, but then an individual is subject, and acts on, these curves. This is fine, as long as we recognize that in doing this we are performing an approximation. The problem is that economic theory often ignores the fact that it is using an approximation: it does not deal with individual-level economics, with the world of single individuals. There is no book of economics where you will find a chapter discussing the behaviour of the supply and demand of a single individual, how noisy they are, how they are statistically distributed over the population... What you will find is an average, and this is then applied to each individual. This way of treating "signals" is a well known approach in science which is called "mean field approximation". The mean field approximation is exactly what it is called: it is an approximation where you substitute a possibly noisy and unknown value with the known average value. In doing so, however, you are neglecting a lot of information. Going beyond mean field theory is a complicated task that requires instruments to connect the individual-level and the market-level descriptions. Given the individual-level is ignored in neoclassic economic theory, you cannot say much about anything that goes beyond the mean field approximation. Economists focus on averages and aggregated values, and typically do not account for anything that goes beyond these approximations.

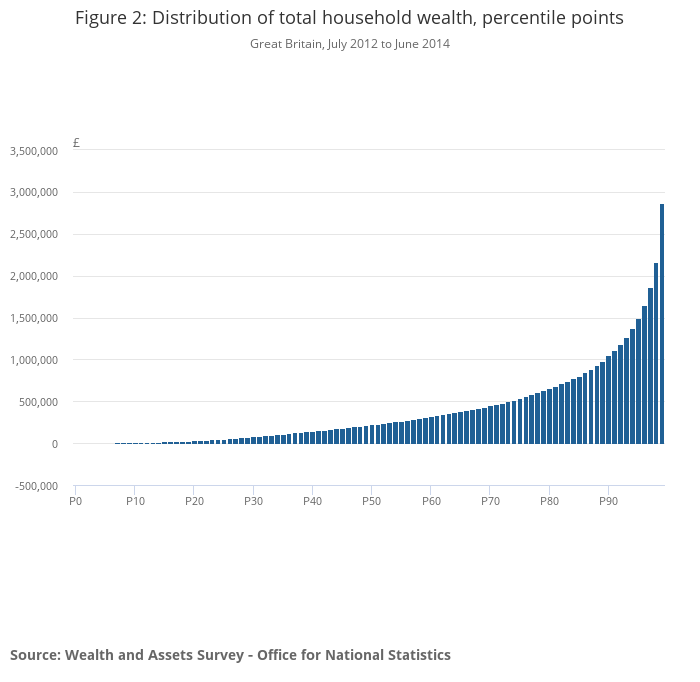

This has profound consequences that are not acknowledged by economic theory. For instance, the world has seen an increase in economic inequality: the typical plot shows that few percents of the population own a large part of the total wealth. In the UK, data between 2012 and 2014 shows that the top 10% of the population owned 43% of the total wealth. The distribution of wealth is shown in the plot below.

The question many economists and the general public have often been debating is the following: can we have a less unequal wealth distribution? The question itself assumes that the plot above shows wealth distribution to be unfair, but how do we know that it is unfair? How is a fair wealth distribution supposed to be? The problem here is that differences in wealth may arise quite easily. Education for one, is a factor that may lead to a difference in income. For instance, some people who make early investment in education and savings, are able to achieve early economic independence. They do this by renouncing to a number of life experiences typical of certain young age groups. Monetary investments are another source of wealth difference. Saving money to invest may lead to difference in wealth at later life stages. The point is that each person has a different relation with investing, whether it be investing in education, investing in certain jobs, or financial investing. We might buy a new expensive car, or buy the cheapest one and invest the remaining money. The choice between these two behaviours determines our wealth later in life. We do not all have the same attitude: we do not necessarily choose jobs that give higher returns, we do not necessarily have an attitude to education: all of this leads to wealth differences.

The point is, how should we expect wealth to be allocated: what is supposed to be "right"? Since our choices will lead to differences in wealth in the long term, should not this be reflected in the wealth distribution? Or should we penalize the money saver because he dared putting money aside for his old age, as I heard once?

A further problem in defining the optimal wealth distribution, is that we are essentially trying to find an equilibrium distribution of wealth within a population, but as all equilibria it will be subject to external factors that are not included in our reasoning: that is all market forces that act over the economic landscape. When inflation hits, the wealth distribution will necessarily change; when the Central Bank rises or lowers interest rates, its directly affecting how credit expansion acts within the economy and, thus, how the wealth will be distributed. Owing to this, it is not at all evident that we can even talk about an optimal wealth distribution, nor that it would be right to try to affect wealth distribution without causing feedback effects in the economy. It is not even clear why should such distribution be modified as we do not know what would make it fair. We are dealing with words, rather than well defined concepts.

At the moment, any discussion regarding this issue is based on the personal, political, and deep-rooted views of the debaters, rather than objective facts. The economic landscape is a reflection of individual choices: if individuals are all perfect copies of one another, with same goals and same capabilities, same choices, then all will behave similarly. We may expect all to get a similar outcome, thus probably some well behaved distribution of wealth that reflects our expectations of the average individual. However, as soon as we introduce different choices, wealth will not be distributed according to our expectations. Economists have been stuck on this issue without finding any objective solution. The problem is that economics does not account for differences at the individual level: it does aim to describe differences at population level in broad categories, but unless it is capable of incorporating individual choice, it will not be able to construct a theory that may answer the question of wealth distribution from an objective standpoint. That is because such a theory is beyond the mean field approximation used in economic theory. Since economics has no notion of individual-level economics, and thus has no concept of "beyond mean-field".